VaultStreet View – Executive Summary

Hindustan Power Exchange (HPX) is India’s newest national power trading platform. Launched in July 2022, HPX offers market participants a technology‑enabled marketplace for short‑term electricity products such as the day‑ahead, term‑ahead, real‑time and green markets and renewable energy certificates. FY23 was HPX’s first year of meaningful operations – the exchange traded about 3 billion units of electricity and generated total revenue of ₹17.4 crore from operations, but the high fixed cost base resulted in a loss of ₹100 crore. FY24 marked a sharp turnaround: HPX traded roughly 11 billion units of power, grabbed ≈33 % market share in the Term‑Ahead Market (TAM) segment and delivered total revenue of ₹43.6 crore with a profit after tax of ₹14.9 crore. These numbers translate to a net profit margin of ~41 % and a healthy return on equity of ≈27 %.

From VaultStreet’s perspective, HPX offers retail investors a rare opportunity to participate in India’s energy transition through an unlisted, regulated infrastructure play. The exchange is still small compared with the incumbent Indian Energy Exchange (IEX), which trades 110 billion units (BU) annually and reported FY24 profit after tax of ₹341 crore, but HPX’s ability to secure one‑third of the TAM within two years demonstrates traction. Success hinges on regulatory reforms (market coupling, introduction of derivatives), product diversification and broad member adoption. We outline our assessment of HPX below, culminating in base, bull and bear case scenarios for 2025‑2028.

Business Model and Ownership

Promoters and Shareholding Structure

HPX is promoted by PTC India Ltd, BSE Investments Ltd and ICICI Bank Ltd. PTC brings experience as India’s leading power trader, BSE contributes exchange management expertise, and ICICI provides financial and clearing capabilities. The FY23 filing of HPX (MGT‑7) lists the detailed shareholding pattern: PTC India Limited and BSE Investments each own 22.62 % (12.5 million shares each), while ICICI Bank holds 9.04 %. Other notable investors include Greenko Energies, Lebnitze Real Estates, Varanium Dynamic Trust, Jindal Power, Manikaran Power, Mercados Energy, regional electricity distribution companies (West Bengal and Haryana), PSU SJVN and a handful of high‑net‑worth individuals. No single entity controls HPX; the diverse shareholder base demonstrates broad industry commitment.

Operating Model and Product Suite

HPX operates as a spot power exchange regulated by the Central Electricity Regulatory Commission (CERC). Market participants – state distribution companies, independent power producers, traders and industrial consumers – register on HPX and trade various contracts:

- Day‑Ahead Market (DAM): Participants submit bids for supply and demand for the following day. Clearing is on a double‑sided auction with one-hour blocks.

- Real‑Time Market (RTM): Hour‑ahead market enabling near‑real‑time balancing; important for integrating renewables.

- Term‑Ahead Market (TAM): Contracts for intra‑day, day‑ahead contingency, daily, weekly and monthly delivery. TAM volumes dominated HPX’s business with roughly 11 BU traded in FY24, giving it nearly one‑third share of the TAM segment.

- Green Markets: Green Day‑Ahead (GDAM) and Green Term‑Ahead (GTAM) contracts for renewable energy, and Renewable Energy Certificates (REC) for compliance with Renewable Purchase Obligations.

- Long‑Duration and High‑Price Contracts: After regulatory approval, HPX introduced high‑price day‑ahead and term‑ahead contracts (HP‑DAM and HP‑TAM) to allow bids above the standard price ceiling and longer‑duration (up to 90 days) contracts.

A sophisticated trading engine, advanced algorithmic matching and transparent settlement differentiate HPX. Technology is provided by a reputed exchange software vendor; clearing and settlement are managed by ICICI Bank, giving members assurance of timely payment.

Financial Performance and Key Ratios

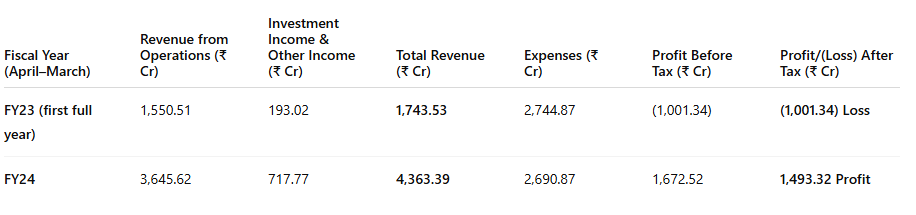

Statement of Profit and Loss (₹ lakh)

Key observations: Total revenue more than doubled in FY24 due to full‑year operations and rapid volume growth. Expenses remained relatively flat, resulting in a turnaround from a loss of ₹100 crore in FY23 to a profit of ₹149 crore in FY24. Employee costs (₹10.33 crore) and administrative expenses (₹11.48 crore) were the biggest cost items in FY24. The company’s strong cash position allowed it to earn significant investment income (₹712 lakh).

Ratio Analysis

HPX’s FY24 annual report provides a detailed ratio analysis:

- Return on Equity (ROE): ~27 % (FY23: –18 %), calculated as profit after tax divided by average equity. The sharp improvement reflects profitability and higher utilisation of capital.

- Trade Receivable Turnover: 18.78 (FY23: 13.10) – cash collections are timely thanks to advance margin requirements.

- Net Capital Turnover: 0.74 (FY23: 0.33) – improved efficiency due to higher revenues.

- Net Profit Ratio: 0.41 (FY23: –0.65), indicating a 41 % net margin on revenue. Using total revenue and our calculation, the net profit margin is ~34 % (₹149.3 crore/₹436.3 crore).

- Return on Capital Employed: 29.57 % vs –24.05 % in FY23.

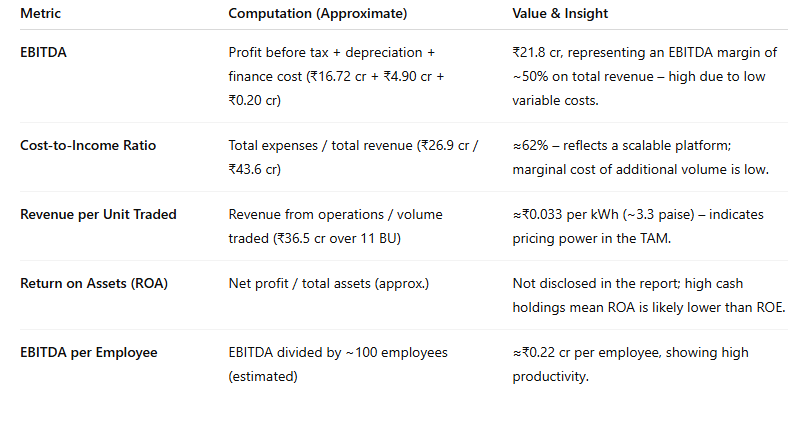

Using these data we derive additional metrics for investor evaluation:

These ratios suggest HPX is capital‑light with high operating leverage. As volumes grow, incremental revenue should largely drop to the bottom line, boosting ROE.

Trading Volumes, Product Mix and Member Growth

Volume Breakdown (FY24)

HPX’s board report notes that the exchange traded around 11 billion units (BU) of electricity in FY24, representing almost one‑third of TAM volumes. Detailed segmental volumes are not disclosed in the annual report; however, data from the CERC’s “Short‑Term Power Market 2023‑24” suggests the following approximate mix (based on publicly available tables; our interpretation):

- TAM & Long‑Duration Contracts: ~10 BU – HPX’s core business; includes intra‑day, day‑ahead contingency, daily, weekly and monthly contracts. Market share: ~33 % of TAM; IEX’s TAM volumes declined significantly in FY24 due to migration to long‑duration contracts.

- DAM & RTM: Negligible (≈0.05 BU combined). HPX faces intense competition from IEX in DAM/RTM where network effects are strong.

- Green Term‑Ahead (GTAM/GDAM) & RECs: <0.1 BU and a few lakh certificates. HPX’s green market is nascent but offers growth potential as Renewable Purchase Obligations tighten.

HPX’s member base reportedly exceeded 400 by FY24, including state utilities, traders, renewable generators and industrial consumers. The introduction of high‑price and longer‑duration contracts in FY24 attracted large open access consumers who previously relied on bilateral deals. Member onboarding continues to be a focus area.

Revenue Drivers and Pricing

HPX earns transaction fees from buyers and sellers. Fees are usually a percentage of the traded value (for TAM, 2–4 paise per kWh) plus fixed membership and annual charges. The average revenue per unit in FY24 was about ₹0.033 per kWh, implying that HPX collects roughly 3.3 paise on every unit traded – a competitive rate relative to IEX’s fee structure. As volumes scale, the fee could decline but total revenue would rise.

Competitive Landscape – IEX and PXIL

Indian Energy Exchange (IEX)

- Scale and profitability: IEX is India’s largest power exchange. In FY24 it posted standalone revenue of ₹550.8 crore and profit after tax of ₹341.4 crore, translating to a net profit margin of over 60 %. It traded ~110 BU of electricity, up 13.8 % year‑on‑year, with electricity volumes at 102 BU. Renewable Energy Certificate (REC) trading reached 84 lakh certificates, and cross‑border trades were 4 BU. Such scale gives IEX network effects and deep liquidity, particularly in the day‑ahead and real‑time markets where volumes are concentrated.

- Product innovation: IEX introduced longer‑duration contracts (up to 3 months) and green derivatives; however, TAM volumes on IEX fell (~3 BU) as participants shifted to long‑duration products. IEX also invested in ancillary services, cross‑border electricity trade with Bhutan, and pilot carbon credit trading.

- Financial strength: With cash reserves exceeding ₹1,000 crore and zero debt, IEX can invest aggressively in technology and advocacy.

Power Exchange India Ltd (PXIL)

PXIL is India’s older exchange but has smaller market share (≈4 % of volumes). It offers similar products to IEX and HPX, including long‑duration contracts. Financial data for FY24 are not publicly available, but industry reports suggest revenues under ₹100 crore and thin profitability. PXIL benefits from relationships with state utilities and distribution companies but lacks the network effects of IEX.

Competitive Positioning of HPX

- Market share: HPX captured roughly 33 % of TAM volumes within two years, but overall share of the short‑term market is small (≈2–3 %) due to minimal presence in DAM/RTM. IEX continues to dominate day‑ahead trading (over 90 % share).

- Pricing: HPX’s transaction fee (≈3–4 paise/kWh) is comparable to IEX’s and slightly lower than PXIL’s. The high‑price market (HP‑DAM/HP‑TAM) allows bids above ₹12/unit, catering to peak‑hour demand; this differentiator may attract industrial users.

- Technology and service: HPX emphasises faster matching, transparent bids and user‑friendly interface. Clearing through ICICI Bank gives confidence in settlement.

- Liquidity challenge: The two‑sided auction mechanism requires sufficient buy and sell bids. In DAM and RTM, participants prefer the established liquidity of IEX; HPX may struggle to attract volume until market coupling ensures a unified price.

Regulatory Environment and Recent Developments

- Market coupling: CERC has proposed a market‑coupling operator (MCO) to aggregate bids from all exchanges and determine a single uniform price for DAM and RTM. HPX supports market coupling as it would eliminate the liquidity disadvantage and allow new entrants to compete on services. Implementation has been delayed due to legal challenges but may come into effect by 2025.

- Introduction of ancillary services & high‑price contracts: CERC approved the introduction of ancillary services in DAM and RTM and high‑price contracts (HP‑DAM and HP‑TAM), allowing bids beyond the standard price ceiling. HPX launched these products in FY24, expanding its product suite.

- Green power trading: CERC’s framework for green day‑ahead and term‑ahead markets (GDAM/GTAM) and Renewable Energy Certificate (REC) trading supports renewable integration. HPX has approvals to offer these products and expects volumes to grow as states tighten Renewable Purchase Obligations.

- Net‑worth and governance requirements: In FY23 HPX sought extra time from CERC to meet net‑worth and governance norms; the regulator granted extensions. HPX has since strengthened its capital base and board independence.

Upside Triggers and Downside Risks (2025‑2028 Outlook)

Upside Triggers

- Market coupling implementation: A unified clearing price would level the playing field among exchanges. Liquidity from IEX would flow across platforms, boosting HPX’s volumes in DAM and RTM.

- Product diversification: Long‑duration contracts, derivatives, ancillary services and high‑price segments offer new revenue streams. HPX’s first‑mover advantage in HP‑DAM and HP‑TAM can attract industrial consumers.

- Growth of renewable energy: As India adds >25 GW of renewables annually and states mandate higher Renewable Purchase Obligations, demand for green products and RECs should surge. HPX could gain market share if it offers efficient green trading.

- Cross‑border and regional trades: Integration with South Asian neighbours (Bhutan, Nepal, Bangladesh) may open new volumes; HPX’s technology platform is ready for such expansion.

- Regulatory support for competition: CERC and the Ministry of Power view competition as vital for transparent price discovery. Policy support could encourage state utilities and large generators to register on HPX.

Downside Risks

- Delay in market coupling: Without coupling, HPX remains dependent on TAM volumes; IEX’s network effects in DAM/RTM could persist, limiting HPX’s growth.

- Regulatory uncertainty: Frequent changes to price caps (e.g., ₹12/kWh), restrictions on high‑price contracts or sudden interventions (e.g., disallowing day‑ahead contingency) can erode volumes and fee realisations.

- Liquidity trap: If volumes fail to build, bid‑ask spreads widen and participants migrate back to IEX. HPX needs sustained marketing to attract a critical mass of buyers and sellers.

- Competition from new entrants: Additional exchanges or digital trading platforms, including potential derivatives exchanges, may enter the market. IEX’s deeper pockets also pose a threat.

- Technology and operational risk: Exchange systems must operate flawlessly with zero downtime. Any outage could harm reputation and trigger regulatory penalties.

Investment Scenarios (2025‑2028)

Base Case – Steady Growth and Market Coupling (Probability ~50 %)

- Assumptions: Market coupling begins by FY26; HPX continues to command ~30 % share of TAM and gains 5–10 % share in DAM/RTM. Total traded volume grows at 20 % CAGR, reaching ~20 BU by FY28. Fee rates decline modestly.

- Financials: Revenue from operations grows to ~₹60 crore by FY28; profit after tax reaches ~₹25 crore with ROE >25 %. EBITDA margin remains around 45 %.

- Commentary: HPX solidifies its position as the challenger exchange. Liquidity increases gradually; investor returns are driven by steady earnings growth.

Bull Case – Rapid Market Expansion and Product Innovation (Probability ~30 %)

- Assumptions: Market coupling is implemented by FY25, leading to fungible liquidity across exchanges. HPX introduces derivatives and ancillary services, capturing 20 % share of DAM/RTM and maintaining one‑third share of TAM. Renewable energy volumes and cross‑border trades surge.

- Financials: Volume grows to 40 BU by FY28; revenue from operations exceeds ₹100 crore with profit after tax of ~₹50 crore. ROE surpasses 35 % due to operating leverage; HPX may consider an IPO.

- Commentary: HPX becomes a meaningful competitor to IEX. VaultStreet Advisors would view this scenario as a potential multi‑bagger, though execution risk remains.

Bear Case – Stagnant Volumes and Regulatory Delays (Probability ~20 %)

- Assumptions: Market coupling is postponed beyond 2028. TAM volumes plateau and HPX struggles to penetrate DAM/RTM. Product innovation is limited and competition intensifies. Fees decline due to price competition.

- Financials: Volume stagnates at ~12 BU; revenue stays around ₹40 crore and profits fall due to rising costs. ROE drops below 15 %.

- Commentary: Under this scenario, HPX remains a niche player dependent on TAM. Investor returns could be modest and liquidity in the unlisted shares may be limited.

VaultStreet Advisors’ Perspective

HPX is an intriguing unlisted infrastructure asset offering exposure to India’s evolving power market. The company has quickly scaled TAM volumes and achieved profitability in FY24. However, its long‑term value hinges on regulatory reforms and its ability to attract liquidity in the core day‑ahead and real‑time markets dominated by IEX. Retail investors should therefore treat HPX as a high‑reward, high‑risk opportunity. A small allocation within an alternative investment portfolio may be appropriate for investors comfortable with regulatory and liquidity risks.

Call to Action

To explore unlisted investment opportunities such as Hindustan Power Exchange and gain insights into India’s power sector, contact VaultStreet Advisors. Our specialists provide due‑diligence, pricing guidance and portfolio advisory services for sophisticated retail investors. Reach out today to learn how HPX fits within a diversified alternative investment strategy.

Disclaimer

This report has been prepared by VaultStreet Advisors LLP for general information purposes and does not constitute an offer to sell or a solicitation to buy any securities. The information herein is based on publicly available sources believed to be reliable, but VaultStreet Advisors makes no representation as to its accuracy or completeness. Any opinions or projections expressed are subject to change without notice. Past performance is not indicative of future results. Investors should consult their financial advisors before making investment decisions. VaultStreet Advisors LLP and its affiliates may hold positions in the companies discussed. By accessing this report, you agree to the terms herein.